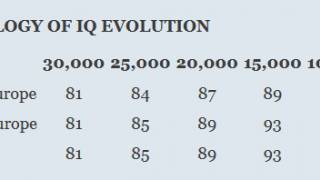

European Stability Mechanism = Debt Slavery

Source: youtube.com

Source: youtube.com

The European Stability Mechanism (ESM) is a permanent rescue funding programme to succeed the temporary European Financial Stability Facility and European Financial Stabilisation Mechanism in the 17-member Eurozone. The ESM is due to be launched as soon as Member States representing 90% of the capital commitments have ratified it, which is expected in July 2012.

Unlimited money supply for the Eurocrats. Where is this money intended to go? Are they building a base on mars?

EU Fiscal Union = EU Debt Serfdom

From: prisonplanet.com

“Fiscal union” is a code-phrase for a highly profitable debt-serfdom: the banks profit, the EU bureaucracy flourishes and the people of the EU are imprisoned in a modern serfdom.

The stock and bond markets are gearing up to celebrate the EU’s approval this Friday of “fiscal union,” the necessary surrender of sovereignty that’s needed to seal the bondage of the EU’s hapless citizenry to the banks and the lapdog bureaucrats slavishly devoted to their dominance.

“Fiscal union” is the code-phrase for the EU nation agreeing to automatic sanctions (penalties) should their borrowing exceed what is deemed prudent. In this sense, it’s little different from the 3% deficit limit that the member states agreed to via the initial treaty but conveniently ignored.

The “teeth” of automatic sanctions is supposed to force nations to “tighten up” their fiscal and tax policies (including collection)–”austerity” at the fundamental economic and governmental levels.

In other words, “Oops, we borrowed too much, default looms, let’s paper over the insolvency by really really really promising to borrow less from now on.”

The mechanisms of the overborrowing–overleveraged, politically dominant banks and the euro–are left untouched. Why? For the “obvious” reasons the mechanisms of EU governance has been captured by the banks and their apparatchiks, and as a result of the quasi-religious devotion of the Eurocrats to the single currency, a catastrophically wrong-headed fantasy that they cannot give up without losing face.

I described the systemic problem with “austerity and higher taxes” as a “solution” to crushing debts in It’s Your Choice, Europe: Rebel Against the Banks or Accept Debt-Serfdom (December 5, 2011): it sets up a positive (mutually-reinforcing) feedback loop where diverting more of the national surplus to pay interest on old debt leaves less for productive investment, a cycle of indenturement to debt that ratchets the risk of default ever higher, which drives interest rates up which then increases the cost of servicing all that crushing debt which then diverts more of the national surplus (via austerity and higher taxes) to paying the higher interest.

Every euro shipped off to the banks and bondholders is a euro that isn’t going to be spent in the national economy, which means the economy contracts from a dearth of investment, income and spending. “Growing our way out of debt” is impossible in this indentured-to-debt positive feedback loop.

In a functioning democracy, then those who reaped the gain (the banks) would actually be exposed to the risk that accompanied their gain. But sadly, the EU is not a democracy except as a simulacrum propped up for PR purposes. The risk and the gain have been neatly separated by the Eurocrats and the toady figurehead leadership (Merkozy et al.).

As a result the gain remains safely private with the banks while the risk and losses are shifted to the taxpayers and citizens of the EU, who must now make good on those stupendous losses while remaining exposed to the risk of future default.

The same is of course also true in the U.S., another facsimile democracy in which the government and its proxies guarantee banks’ profits and leverage while transferring the risk and losses to the voiceless taxpayers. (Go try to cast a vote over Fed policy. Serf, meet your Overlord, Ben Bernanke).

The banks and their lackeys in government prefer to use unaccountable proxy agencies to do the heavy lifting–the European Central Bank (ECB), the Federal Reserve, and the European Financial Stability Facility (EFSF), which is soon to be joined with other alphabet-soup agencies of oppression and predation, all in the name of “rescue.”

Rescuing who and what? The banks and bondholders, of course. This requires avoiding not just democracy but also capitalism, which would require the clearing of bad debt via the discovery of price of both debt and risk, and also socialism, which would require wiping out the wealth of the banks and bondholders via nationalization, a process that would at least return surviving assets and control to an elected government.

It’s not democracy, capitalism or socialism–it’s all opacity and artifice to mask the imposition of a new, improved debt-serfdom on Europe, all in the name of “fiscal unity.”

The eurocrats and the toady leadership would be more honest were they to simply declare: “We had to destroy democracy to save the banks. You are now serfs in our financial fiefdoms.”

From: prisonplanet.com